Proactive Ways to Beat the Cost of Living Crisis The cost of living crisis has […]

5 min read

1

Life on the ranch with Blissful Mrs. Mimi — a assistant principal blogging about animals, country living, and the joyful chaos of fluffy and feathery friends.

Proactive Ways to Beat the Cost of Living Crisis The cost of living crisis has […]

How To Avoid Money Worries After An Injury A serious injury can change your life […]

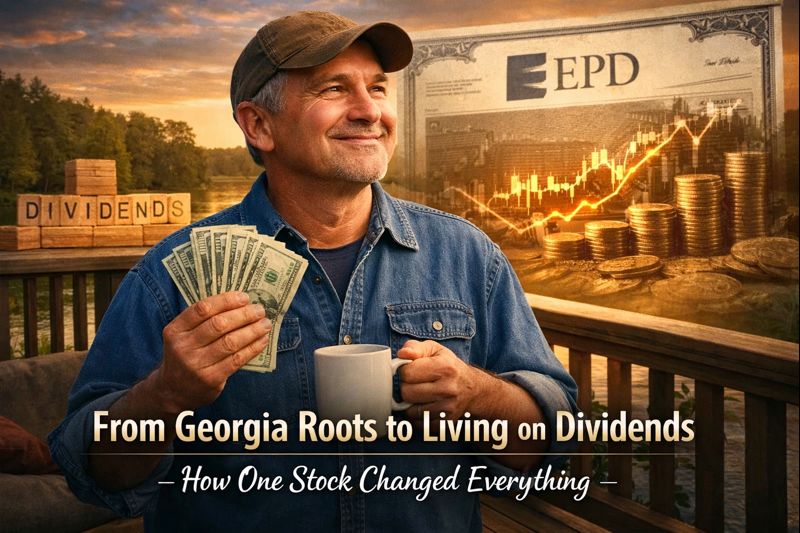

From Georgia Roots to Living on Dividends: How One Stock Changed Everything I grew up […]

4 Ways To Boost Your Savings With Change. When you’re trying to save money, drawing […]

Money management gets very hard sometimes, and often enough we struggle to see a way […]

How To Prepare For Your Family’s Future. If you have just started a family, then […]

Being able to make good financial decisions doesn’t just happen. We have to teach our […]

Your Finances Don’t Have To Suffer From These Things. It might not be […]

How You Can Get Through A Wonderful Holiday On A Budget When you think about […]